This article is about Justworks PEO. What product am I using?

First passed as part of the CARES Act on March 27, 2020, the Employee Retention Tax Credit (ERTC) helps employers keep employees on payroll by providing tax credits based on qualified wages. To ensure that your business is taking full advantage of the relief offered by ERTC, we also encourage you to talk about this program with your accountant and or tax advisor.

ERTC applies to wages paid from Q2 2020 through Q4 2021. There are different ways to qualify which changes eligibility for certain quarters. For 2020, the credit is 50% of qualified wages paid to employees, up to a maximum of $10,000 per employee for the year. This means the maximum credit is $5,000 per employee for all eligible expenses paid in 2020. For 2021, the credit increased to 70% of qualified wages, up to $10,000 per employee per quarter. This results in a potential maximum credit of $28,000 per employee for the year.

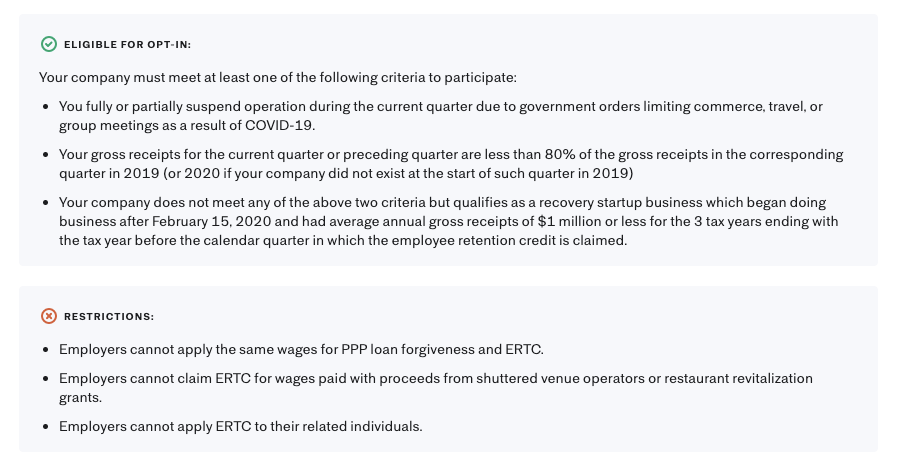

There are three different categories to qualify. The first two categories are operational disruption and revenue decline, and apply for Q2 2020 through Q3 2021.

- Operational disruption: Businesses must have experienced a full or partial suspension of operations due to government orders related to COVID-19

- Revenue decline: A significant decline in gross receipts compared to the same quarter in the previous year. For 2020, this decline must be more than 50%, and for 2021, more than 20%

The third way to qualify is to be considered a recovery startup business (RSB). RSBs only qualify for credits related to Q3 and Q4 2021, and have a maximum credit of $50,000 per quarter.

- Recovery startup business- A company that was incorporated on or after February 15, 2020 and has qualifying wages in Q3 and Q4 2021.

Note: If your company has related entities, you may have to include those entities when you consider your company’s eligibility.

It’s your responsibility to maintain records sufficient to substantiate eligibility for the Employee Retention Tax Credit, such as documentation sufficient to demonstrate that your company’s gross receipts declined by the requisite amounts.

ERTC and PPP Loans

Initially, businesses that received Paycheck Protection Program (PPP) loans were not eligible for the ERTC. However, subsequent legislation, such as the Consolidated Appropriations Act of 2021, allowed businesses to claim both the PPP loan and the ERTC, but not on the same wages. We recommend speaking with your tax advisor if you received a PPP loan and believe you also qualify for ERTC.

The deadline to submit ERTC to the IRS for 2020 quarters was April 15, 2024. Justworks is no longer accepting submissions related to 2020 wages. The final deadline to submit documents for eligible 2021 ERTC claims to Justworks has been extended to November 8, 2024.

On September 14, 2023 the IRS put a moratorium in place which halted further processing of ERTC claims through December 31, 2023. This has led to a backlog of returns and a delay in processing amendments, which in turn has resulted in longer wait times to receive credits. This moratorium did not put an end to submitting claims; however, on January 19, 2024, the House of Representatives announced a bipartisan agreement on tax legislation that, if enacted, would set a final deadline of January 31, 2024, for ERTC submissions. On August 1, 2024, this bill was brought to vote on the Senate floor and was voted down.

How do I submit ERTC claims to Justworks?

If you believe you qualify for ERTC for any quarters in 2021 please reach out to the Customer Support team at Justworks to be provided the attestation to submit your claim. The attestation will be completed through Docusign. All submissions must be received by November 8, 2024.

You will be provided two options. Option A, you provide the signed attestation and your own ERTC calculation, which will be reviewed by Justworks. Option B, you select Justworks to calculate the credit amounts for you.

If you select Option A (provide your own calculation), we will ask you a few more questions to complete the attestation:

- The eligibility criteria you qualify under (decline in gross receipts, suspended operations, or recovery startup business)

- If you selected suspended operations, you will need to indicate if your operations were fully suspended, partially suspended, and/or if it meets the 10% reduction in ability to provide goods and services for one or more quarters.

- We will also need a file breaking out the ERTC calculation by employee, by expense, by quarter. You will also need to include the allocation of PPP loan funds used to pay for each employee.

If you select Option B, we will ask you a few more questions to complete the attestation:

- The eligibility criteria you qualify under (decline in gross receipts, suspended operations, or recovery startup business) and applicable dates

- If you averaged less than 500 employees in 2019

- If you (together with any related entities covered by the IRS’s aggregation rules) averaged above 500 employees in 2019, you will not be able to proceed at this time.

- If there were any “related individuals” employed by the company

- If any individual owned more than 50% of the company

- If the company is considered a non-profit, foundation, or 501(c)(3)

- If the company received a PPP loan and dates if applicable

- You cannot claim ERTC credits on wages that you will also use on your application for loan forgiveness under the Paycheck Protection Program (PPP).

- If you have received a PPP loan in 2021, we’ll ask you some additional questions about the Covered Period of your PPP loan for your loan forgiveness application.

- During the Covered Period that you enter, we will not apply ERTC credits.

- By SBA rules, your Covered Period starts on either the date you receive your PPP funds or the first day of the next pay period following that date.

- You should then enter an end date that is between 8 and 24 weeks from the start date that you enter, depending on your needs with respect to your loan forgiveness application.

- If you’re not sure about your Covered Period, we recommend discussing with your tax advisor before completing ERTC enrollment.

As a reminder it is your responsibility to maintain records sufficient to substantiate eligibility for the Employee Retention Tax Credit, such as documentation sufficient to demonstrate that your company’s gross receipts declined by the requisite amounts.

How do I know if I am eligible for ERTC?

Justworks does not determine eligibility for ERTC as we are not allowed to provide legal or tax advice. If you are unsure of your eligibility, contact your tax or legal advisor.

How does this work with FFCRA?

If you have employees on FFCRA leave and also opt into the employee retention tax credit, Justworks will make sure you’re not being credited for the same wages to avoid tax penalties. If you added an employer contribution to FFCRA leave, that amount will be eligible for a tax credit. For more info, visit the IRS’ FAQs on the employee retention tax credit.

How does this work with related entities?

Under IRS guidance, certain related entities may be considered a single employer for retention tax credit eligibility questions, including whether an employer meets the economic conditions set forth above, has received a PPP loan or is under the applicable average employee thresholds. Visit the IRS FAQS for specific guidelines around aggregation rules and determining employer eligibility.

Disclaimer

This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, legal or tax advice. If you have any legal or tax questions regarding this content or related issues, then you should consult with your professional legal or tax advisor.